Institute of Customer Service response to Financial Conduct Authority consultation CP15/41: Increasing transparency and engagement at renewal in general insurance markets

The Institute of Customer Service is an independent not for profit professional membership body, with over 500 organisational members. Our purpose is to help organisations strengthen their business performance by focusing on raising the standards of their customer experience which in turn will improve their customers’ experiences.

Overview

The Institute of Customer Service welcomes the opportunity to comment on this consultation. Our research shows that openness and transparency is of increasing importance to consumers and that businesses should see these as a key driver of their relationship with their customers. There is a clear correlation between customer satisfaction and trust.[1]

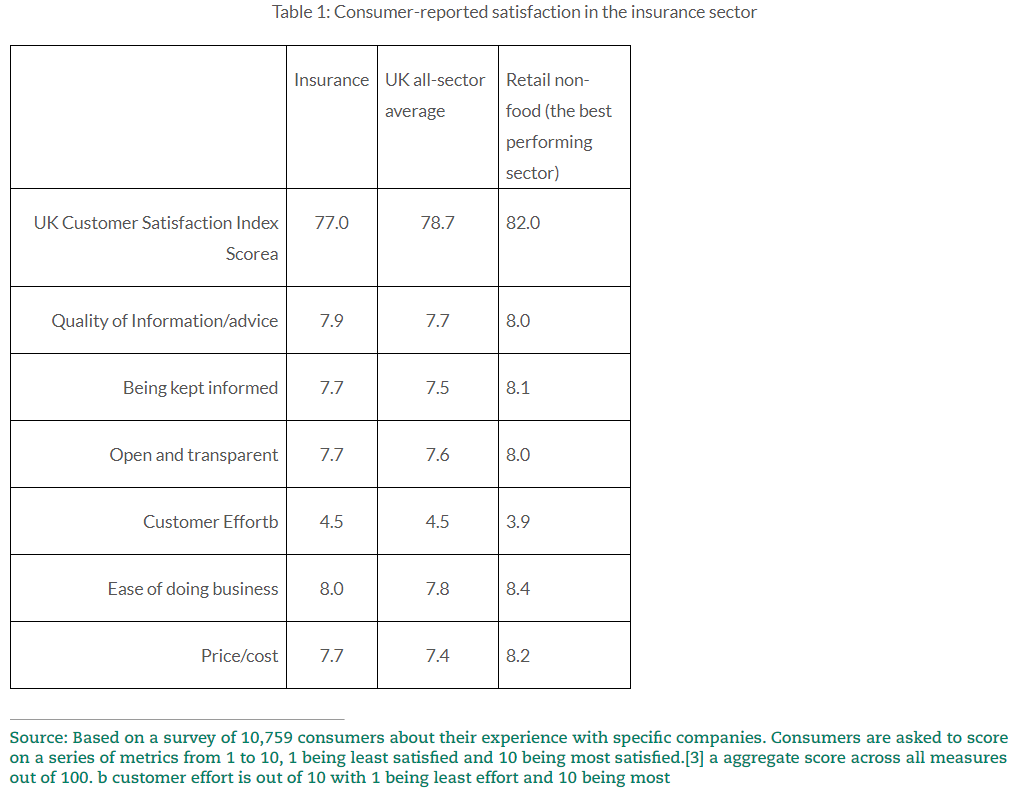

Customer satisfaction for the insurance sector has increased by 1.6 points compared to January 2015. Consumers now score satisfaction with insurance firms at 78.7 (out of 100), which is 1.7 points above the all-sector average in the UK Customer Satisfaction Index, and the sector ranks sixth out of the 13 sectors (see Table 1 below). This shows there is room for improvement and we welcome this consultation in raising the issue openness and transparency and the way information is provided to consumers in the insurance sector.

However, we do not think that the proposals in the consultation and in particular the creation a very specific and prescriptive binding rule will provide the best outcome for consumers or firms. The existing rules are sufficient to require firms to provide appropriate information on premiums at renewal. The FCA should instead focus on producing non-handbook guidance to provide resources and encouragement to firms to properly engage with their customers, including best practice and learning from other sectors. This is the best way to ensure properly informed and empowered consumers and customer-centric firms.

Questions

Q1. Do you agree with our proposal that firms should disclose last year’s premium on renewal notices?

No. We think providing clear and open information to consumers is good for both consumers and businesses but that regulation is the wrong way to achieve this and that the proposals of the FCA are too prescriptive. In addition, by focusing on only to one aspect of communication these proposals fail to address the wider issue of customer engagement.

What consumers think

Our research shows that whilst the insurance sector performs well compared to other sectors in consumer-reported satisfaction in terms of the quality of information and advice given, keeping customers informed and being open and transparent there is still room for improvement (see Table 1 below).

Most people make contact with insurance companies to get a quote or look at the offering (29.8%) and satisfaction is high for this contact and ahead of the all sector average (80.7 and 78.8 respectively). The second most common reason people made contact was to make a purchase (26.3%) and again satisfaction is high and close the all sector average (79.8 and 80.0 respectively).[2]

Whilst overall satisfaction for these interactions was high, our research also looks at what consumer’s value in their interaction with firms. This shows that amongst other things they value the quality of information and advice, being kept informed and, openness and transparency. The sector does not perform as well on these measures as other parts of the economy (for example compare to the retail sector in Table 1 below.) The research also shows that the sector can do more to be easier to do business with and reduce the effort for customers engaging with firms.

How the FCA should achieve better information for consumers at renewal

Given our research findings, we think there is great value in the principle of the consultation proposals and we welcome the research the FCA has done on this and the suggestions made. However, we do not think imposing this very specific requirement via a rule is an appropriate course of action. The current rules are sufficient and imposing the proposed obligations is too prescriptive and will restrict the development of a wider business-customer relationship. There is a need to encourage wider transparency across a range of contact points. We believe that the FCA should provide further non-handbook guidance around information displayed on renewal notices.

We think that the existing obligations under Principle 6 and 7[4] and under information rule ICOBS 6.1.5[5] are sufficient regulatory requirements on firms in relation to information provision. In particular, we think that in order to be providing ‘appropriate information’ in a ‘comprehensible form’ as required by ICOBS 6.1.5 firms should be providing clear comparison information about their renewal premium. This could, however, be made clearer through further non-statutory guidance and further action only considered after the FCA has monitored the impact of highlighting these issues.

In addition, we think that the particular proposal the FCA settled on is a very prescriptive considering the wider policy objective identified. The FCA should revisit some of the options it dismissed before the trail stage as some of these, and possibly options not considered, may have value (see below for a discussion of the options). This is another reason why further non-handbook guidance would be most appropriate. The FCA can lay out a series of options and its research and allow firms to innovate on the best ways to communicate with customers to achieve their regulatory obligations. We think this would be preferable to prescriptive regulation.

What better information for consumers looks like

We encourage the FCA to look at practice outside the sector when considering issues around service to customers. We note that the FCA considered alternative proposals but dismissed them before the trial on the grounds that they may be ‘confusing for consumers, introduce practical implementation difficulties and higher costs for firms and give rise to potential unintended consequences.’

Whilst we welcome the caution in imposing requirements that are not customer-friendly or would create unnecessarily burdensome regulation, we are concerned that other options may have been dismissed too early and that experience by other sector regulators may have provided evidence of their usefulness. For example, the options of requiring the disclosure of ‘new business equivalent premiums or the lowest premium over time’ we not pursued. These options are similar, however, to the requirements on suppliers in the energy sector to inform customers on their bills if they could save money by switching to another tariff.

There are also other possibilities not considered. For example, it could be useful for those consumers who had renewed their premium multiple times if the price of the premium the consumer had when they first bought the product is disclosed (please see our response to Question 4 below).

The potential usefulness of these other options demonstrates the problem with the prescriptive approach taken by the FCA. By specifying the form further information takes a new rule will mean firms do not seek out the best way to provide useful, appropriate and comprehensible information to customers to enable them to make the best decision. A new rule could create a compliance driven or tick box approach to providing information to customers rather than genuine engagement in customer needs.

The FCA should consider revisiting some of the options it dismissed and all sector regulators should work together to share research, learning and best practice particularly on an important cross-cutting issues like service to customers. We acknowledge that there may be sector-specific considerations but the expectations of customers are increasingly consistent across sectors. Consumers do not restrict their thinking to a single sector when considering service issues and could reasonably wonder why they receive certain information about a product in one sector but not in other sectors.

What businesses should do

Businesses should be encouraged to provide appropriate and comprehensible information to consumers not only because it is good for consumers but because it will benefit firms by improving their relationship with their customers and, therefore, ultimately their business performance.

It is important that firms are clear and straightforward in their communication with customers as this is an essential part of building a relationship of trust. Research by The Institute of Customer Service demonstrates that customer satisfaction, loyalty, recommendation and trust are highly correlated. For example, of customers who score an organisation between 8 and 9 out of 10 for customer satisfaction, 44% give that organisation a 9 or 10 out 10 in terms of trust. This rises to 90% if the customer scores them between 9 and 10 out of 10 for customer satisfaction. The implication is that the highest levels of trust and satisfaction are highly related and that these are then related to high levels of customer loyalty and recommendation.[6]

In a service economy increasingly built around relationships between businesses and consumers, rather than just transactions, this is an important insight. It demonstrates that firms should ensure customer service is an integral part of their business strategies.

The focus for the FCA in these proposals is ensuring that consumers are receiving a competitive product in terms of price. This is important but our research shows that whilst 14% of customers seek the cheapest possible deals and will sacrifice levels of service to achieve them, 62% of customers want a balance of price and service with at least a minimum threshold standard of service. A further 23% indicate a preference for excellent service, even if it costs more.[7] This demonstrates that there wider advantages to improving information to consumers because many will respond positively to the improvement in the service they receive.

These insights, on consumer attitudes to both trust and price, highlight that very specific changes like the ones contained in the FCA proposals will not be enough to ensure better outcomes for consumers. Firms themselves need to think more broadly about how they communicate with their customers. They should ensure customer service is a central part of their corporate strategies as this is the only way to ensure proper service for consumers and drive long term sustained business performance.

The FCA can support this by providing research findings and encouraging shared learning between sectors as part of non-handbook guidance.

Q2: Do you agree with our proposal that the premium displayed should be the premium the consumer started the year with, but that firms can include other information, such as mid-term adjustments?

No. As noted above in response to Question 1 we do not think a rule should be created requiring firms to display previous premiums. We do think that this practice, or something similar, is one that firms should adopt and that non-handbook guidance could include the recommendation that a premium the consumer started the year with should be displayed.

Q3: Do you agree with our proposal that firms should also provide information to consumers to check the proposed policy continues to meet their needs and to shop around?

No. As noted above in response to Question 1 we do not think a rule should be created requiring firms to display previous premiums. However, we do think that this is a practice that firms should adopt and that non-handbook guidance could include the recommendation firms provide a statement encouraging consumers to check whether the cover offered still meets their needs.

Q4: Do you have any comments about this additional disclosure? Do you have any suggestions for the proposed message to consumers?

As noted above in response to Question 1 we do not think a rule should be created requiring firms to display previous premiums.

We agree that the proposed message is a useful way of highlighting to consumers the length of time they have remained with a provider and that this could be included in non-handbook guidance. However, we note the proposed message does not necessarily mean the consumer will appreciate the cumulative impact of price increases over the preceding five renewals. We suggest a more appropriate mechanism would be to suggest not only the inclusion of the premium the consumer started the year with but the premium the consumer had when they first bought the product. We think this would provide a greater impetus to the consumer to consider other products.

Q5: Do you have any comments on how the disclosure should be presented to the customer?

As noted above in response to Question 1 we do not think a rule should be created requiring firms to display previous premiums.

We do think that non-handbook guidance could make recommendations as to where any further information about previous premiums is displayed. Any disclosure needs to be prominent in order for it to be useful. However, rather than considering on which page the disclosure is positioned, its position relative to the renewal quote is what the most significant consideration in allowing for comparison. We think that non-handbook guidance could suggest the previous premium (or other information) should be displayed immediately adjacent to, under or above the renewal quote.

Q6: Do you agree with the proposal to apply the measure to all situations where a general insurance policy is renewed with a retail consumer with the exception of policies with a term of less than a year?

No. As noted above in response to Question 1 we do not think a rule should be created requiring firms to display previous premiums.

We do think that non-handbook guidance could make the recommendation that previous premiums only need to be displayed for polices of one year or more.

Q7: Do you have any comments about our proposed implementation of 1 January 2017 for the disclosure measures?

As noted above in response to Question 1 we do not think a rule should be created requiring firms to display previous premiums. We believe that non-handbook guidance should be implemented as soon as reasonably possible.

Q8: Do you have any comments on the proposed non-Handbook guidance?

As noted throughout our response, we think that all of the proposed information provision by firms should be outlined in non-handbook guidance. This is the best way to achieve proper engagement from firms about communication with customers.

However, we welcome the draft guidance produced in the consultation as far as it goes.

Q9: Do you have any comments on our cost benefit analysis (CBA)? (Note: see Annex 2)

No.

[1] The Institute of Customer Service, UK Customer Satisfaction Index – The state of customer satisfaction in the UK (January 2016), p36-37,42-43

[2] The Institute of Customer Service, UK Customer Satisfaction Index – Insurance Sector Results (January 2016), p12

[3] The Institute of Customer Service, UK Customer Satisfaction Index – Insurance Sector Results (January 2016), p8-9

[4] Financial Conduct Authority, Principles for Businesses, (2014). PRIN 2.1 – Principle 6 Customers’ interests and Principle 7 Communications with clients.

[5] Financial Conduct Authority, Insurance: Conduct of Business sourcebook, (2008). ICOBS 6.1.5.

[6] The Institute of Customer Service, UK Customer Satisfaction Index – The state of customer satisfaction in the UK (January 2016), p23

[7] UK Customer Satisfaction Index – The state of customer satisfaction in the UK – January 2015. The Institute of Customer Service, (January 2015). Summary Report, p10

Related Posts

Comments (0)